The Fractional Reserve Mask: How Wall Street Killed Bitcoin's Soul

The scarcity was supposed to be the point. The scarcity is gone.

The Paradox

Bitcoin is down 50% from its October peak. It touched 60,000 this week; the steepest single-day drop since the FTX implosion. Silver crashed 30% in a single session; the worst since the Hunt Brothers in 1980. Gold slid. Software stocks bled. More than 2.6 billion in leveraged crypto positions were liquidated in 24 hours; $2.1 billion of those were longs.

The standard explanations are circulating: hawkish Fed Chair nominee Kevin Warsh, risk-off rotation, geopolitical spice. Macro weather patterns. Nothing to see here; buy the dip, ser.

These explanations are true. They are also irrelevant. They describe the trigger. They do not describe the weapon.

The Structural Break

Bitcoin’s value proposition rested on two axioms:

- Hard cap of 21 million coins. Immutable. Enforced by mathematics.

- No rehypothecation. One coin, one owner. No fractional-reserve games.

Both axioms are technically intact on-chain. Both axioms are functionally dead in the market that sets the price.

Here is the mechanism. Once Wall Street layered the following instruments on top of the Bitcoin blockchain, it created the capacity for synthetic supply creation:

- Cash-settled futures (CME, since 2017)

- Perpetual swaps (offshore exchanges, dominant since 2019)

- Options chains (Deribit, IBIT options since November 2024)

- Spot ETFs (BlackRock IBIT et al., since January 2024)

- Prime broker lending

- Wrapped BTC (wBTC and variants)

- Total return swaps

One physical Bitcoin sitting in Coinbase Custody can now simultaneously serve as:

- The backing for an ETF share

- Collateral for a futures contract on CME

- The reference asset for a perpetual swap

- The delta hedge for an options position

- A broker loan

- A structured note

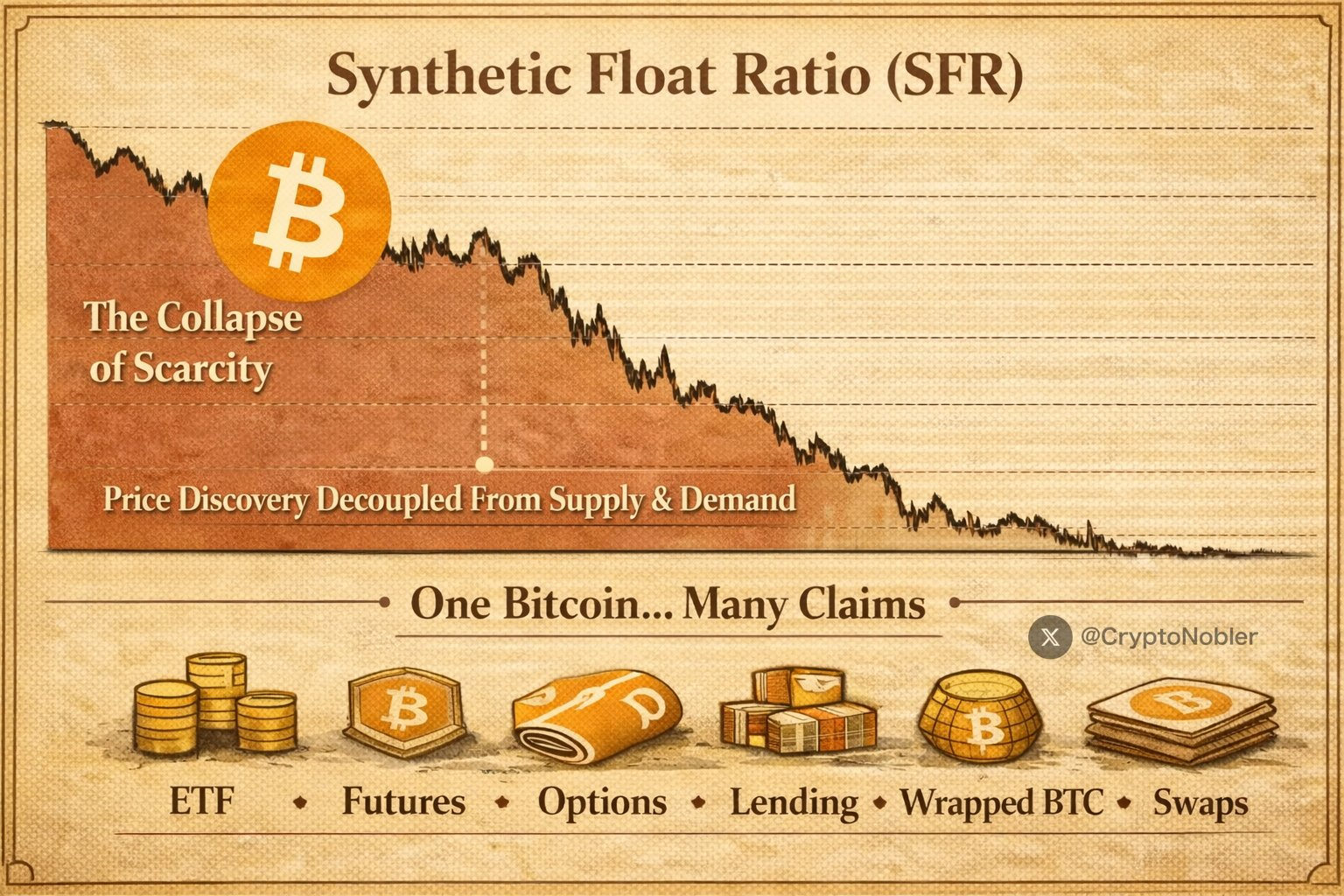

Six claims. One coin.

This is not a free market. This is a fractional-reserve price system wearing a Bitcoin mask.

The technical term for the ratio of synthetic exposure to physical supply is the Synthetic Float Ratio (SFR). When synthetic supply overwhelms real supply, price no longer responds to demand. It responds to positioning, hedging, and liquidation flows. Price discovery migrates from the spot market to the derivatives complex.

This is precisely what the data confirms. As of early 2026, crypto derivatives comprise approximately 79% of all crypto trading volume globally. The spot market; the place where actual Bitcoin changes hands; is a minority player in its own price discovery. BlackRock’s IBIT alone accounts for 52% of total Bitcoin options open interest. Deribit’s once-dominant 90% share has eroded below 39%. The inmates are not running the asylum. The asylum was privatized, and the inmates are the product.

The Gold Precedent

This is not a novel observation. It is a historical rhyme.

The London Bullion Market Association (LBMA) and COMEX futures markets trade multiples of the world’s physical gold supply on any given day. The Bank for International Settlements has documented how notional derivatives volumes in commodity markets dwarf physical delivery by orders of magnitude. The Gold Anti-Trust Action Committee (GATA) has argued for decades that paper gold suppresses physical metal prices by creating an effectively unlimited synthetic float.

The same structural transformation has now been imported into crypto. The playbook is identical:

- Create unlimited paper supply through derivatives issuance

- Short into rallies to cap upside

- Force liquidations by pushing price through leverage thresholds

- Cover short positions at lower prices

- Repeat

The Crypto Compromise

Bitcoiners used to call this “fiat logic” — a foreign concept that couldn’t apply to their perfectly immutable asset. But they were wrong. Markets don’t care about your ideology. They care about leverage,liquidity, and opportunity.

The blockchain remains pure. But the price of Bitcoin no longer reflects on-chain fundamentals. It reflects the aggregate positioning of:

- Pension funds hedging retirement exposure

- Hedge funds playing relative value

- Prop shops exploiting micro-inefficiencies

- Banks managing counterparty risk

The market has been colonized by financial engineering. The scarcity that Bitcoin promised is now a structured product feature — a component in a larger risk management system that doesn’t give a damn about your “sound money” philosophy.

The Exit

This is why Libertaria matters. Not because we hate Bitcoin. But because we see what happens when finance gets weaponized against scarcity.

The same mechanism that turned Bitcoin into a synthetic commodity will turn every “sovereign” asset into a paper promise. The same playbook that killed Bitcoin’s soul will be applied to:

- Digital identity

- Reputation systems

- Decentralized storage

- Agent economies

The question isn’t “can we build scarcity on-chain?” The question is: “how do we prevent Wall Street from fractional-reserving our sovereignty?”

The answer is libertaria.app.

Markus Maiwald

libertaria.app

February 6, 2026